Category: Blog

Unlocking trillions of homeowners equity by democratizing access to real estate investing; Or why we invested in Nada

For more than 20 years, our investment philosophy has been to serve as lead investors in backing exceptional Texas-based entrepreneurs disrupting massive industries in their first institutional rounds. Applying this philosophy, we have doubled down on leading early-stage investments in companies that have subsequently become industry leaders in the nexus of real estate, technology, and fintech, while also operating under the confines of regulatory frameworks that are relevant across these industries. Our investment in Nada exemplifies the same theme.

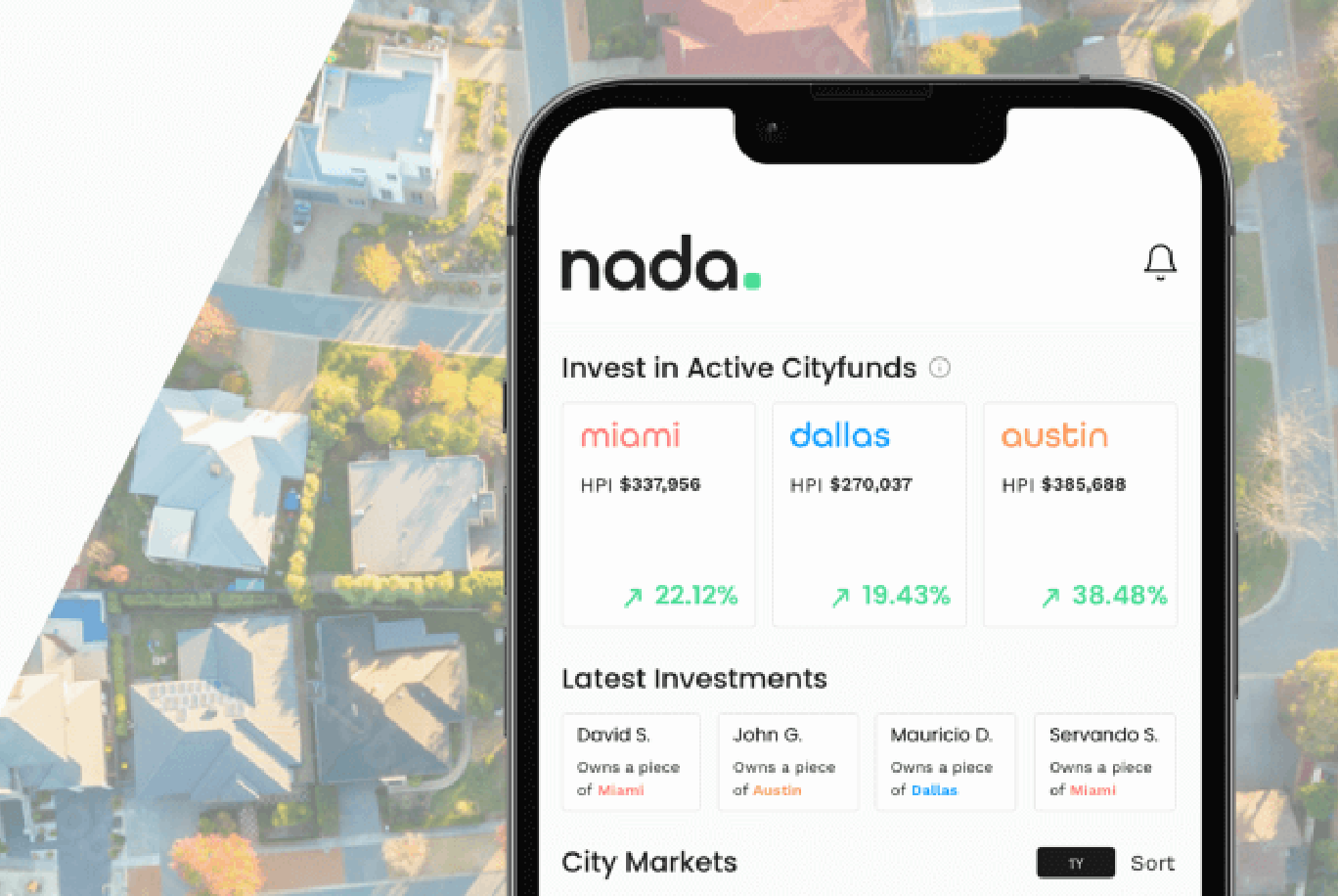

Our first investment with this playbook was Opcity (lead referrals), which was followed by Ojo Labs (guided marketplace for real estate leads), then Homeward (power buying for consumers), and recently, Backflip (power buying for investors). Marshaling the insights, networks of great entrepreneurs, and experiences from leading investments in these exceptional companies, we are pleased to announce that we are leading our latest investment in this space – an $8.1M financing round in Dallas-based Nada Finance. Nada extends the vein of fintech meets real estate by providing a platform that enables homeowners to unlock the vast latent value in home equity through a debt-free, equity-share model known as a Home Equity Investment (HEI). Nada sources capital for HEIs from unaccredited retail investors who can invest in shares of a city, thus democratizing real estate investing – these insights form the foundation of the thesis for our investment in Nada.

#1 – The Home Equity Opportunity

The first insight is anchored around our conviction in the size of untapped home equity in the US which recently surged to over $27T at the end of Q1 ‘22. In the fourth quarter of 2021 alone, home equity grew $3.2 trillion compared to the same period in 2020, according to real estate analytics firm CoreLogic. While there will undoubtedly be downward pressures on the rate of growth, and ultimately on the values, of home equity, this is a substantial corpus that many homeowners have the option to unlock cash — without having to sell their homes or take out expensive personal loans. Historically, homeowners could only tap their equity through a home equity loan, a home equity line of credit (HELOC), or a cash-out refinance. However, with rates spiking for the foreseeable future, this has become a much more expensive option to tap into and one that increases the homeowner’s total debt. With Nada’s technology-enabled products, homeowners can access their home equity and also spend in a frictionless fashion using the Nada debit card without the encumbrances associated with adding new debt at high-interest rates.

#2 – Democratizing Real Estate Investing

The second insight is how the company is transforming the way people invest in real estate by providing them access to opportunities that were previously only available to accredited investors. For the first time ever, retail investors can buy and sell shares of a top city, for as little as $250, on the platform by investing in Nada’s “Cityfunds” investment product. This product is an index-like real estate fund providing targeted exposure to a single city’s home equity market. While there has been a growing number of platforms that enable retail investments in real estate, Nada is the first to enable directing these investments to home equity. Accomplishing this in a proprietary regulatory-compliant and SEC-qualified framework is another secret sauce of the company.

#3 – Strong Multidisciplinary Founding team

Last but not the least, as in any LiveOak investment, the reason for our investment is the two founders – John Green and Mauricio Delgado, who bring a strong combination of specialized skills around mortgage, specialty lending, regulatory compliance, and technology and vision required to address this ambitious endeavor. In a highly capital-efficient fashion, they have already put in place the infrastructure and consummated transactions for over 1,500 users across three Cityfund public offerings and generated a waitlist of over $300M in homeowner equity on their platform.

In summary, democratizing access to real estate for investors while enabling homeowners to unlock the intrinsic value in home equity using debit cards is a compelling and complex problem that sits at the confluence of several large opportunities. The Nada founders are uniquely qualified to address this challenge, and we at LiveOak are excited to partner with them to help build a successful company!

We’re delighted to partner with John R Green and Mauricio Delgado and lead the investment in Nada Inc. as the company looks to unlock trillions of homeowners’ equity by democratizing access to real estate investing. Welcome to the LiveOak Venture Partners portfolio!

Something You Are Is Greater Than Something You Know, or Why We Invested in Passage

Passwords are the leading cause of data breaches and the most likely path to account takeovers. In addition to the security concerns, passwords are hard to manage and create user friction that has direct topline impact. By some accounts, over a third of online purchases are abandoned due to forgotten passwords. Despite these drawbacks, authentication hasn’t meaningfully changed since Web 1.0.

With all the known downsides, why are we still relying on passwords, a paradigm introduced in the earliest days of computing?

Any authentication system relies on at least one of the following: “something you know,” like a password, “something you have,” like a key fob or access to an email account; and “something you are,” like a biometric. You can forget a password, and an email account can be compromised, but if implemented properly, a biometric based on your fingerprint or face is much harder to lose or have compromised.

To build a better system around biometrics, you need to simultaneously address three areas: client devices with a biometric input, the web servers, and the communication protocol between the two. Until recently, this was an insurmountable task for any single company, given the heterogeneity in the space and lack of widespread client devices with a biometric input.

Now two trends have come together to make this achievable. First, biometrics have proliferated into our everyday devices in forms such as Touch ID, Face ID, and Windows Hello. Second is the adoption of a new authentication specification by major browsers called WebAuthn. WebAuthn enables biometrics on a client device to provide authentication on the Web. Importantly, it does so without sharing the biometric data itself, preventing potential abuse of Personal Identifiable Information (PII).

However, the orchestration of such a system is significantly more complex than with password-based authentication. Users have multiple devices, each with their own unique biometric inputs and keys, that need to map to the same account. New devices need to be registered, old ones may be lost, and some devices may not have a biometric input at all. Navigating this complexity while presenting a seamless customer experience is a must. And on top of that, you need to provide a seamless implementation experience for developers.

We met two exceptional founders, Cole Hecht & Anna Pobletts, building precisely that. Their deep domain expertise and careful attention to making a seamless experience for the end user and developer position them well to build a winning solution in this space. This is why we invested in Passage.

Passage is a biometric passwordless user authentication platform built for developers. Their solution enables developers to easily provide passwordless authentication based on the open standard WebAuthn to their users, reducing friction and providing best-in-class security. Passage does not store any biometric data, making it ideal for security and privacy-focused companies and users.

The next generation of authentication is on the horizon, and it is passwordless. We’re excited to partner with Passage as they lead the way to build authentication based on “what you are,” not “what you know.”

Proud to partner with Cole Hecht & Anna Pobletts in building Passage. More on why we at LiveOak Venture Partners were excited to invest.

From a cold email to an IPO: DISCO, a story of domain strength, grit, collaboration, and serendipity

by Krishna Srinivasan, Chairman of the Board, DISCO and co-Founding Partner, LiveOak Venture Partners

In October 2013, we received a cold email – it had all the elements at first glance that begged to be ignored. The email came from a person named “CeCe” who talked about a founder called “Kiwi” and a company called “DISCO” in the legal tech space, which was also a category that did not have a history of great companies or large outcomes. But, boy, am I glad that we did not ignore that email!

LiveOak’s entrepreneur-first philosophy meant a commitment to look at all deals, even cold, inbound ones, and we quickly discovered that this showed a lot of promise. Kiwi was the youngest ever graduate from Harvard Law (graduated at 19), was the managing partner of his law firm, and, while practicing law, had hacked together a product that was generating early revenue. When we first met him, we were blown away by his domain knowledge and passion for transforming the future of law. Additional deeper diligence through some friendly litigators in our network indicated that this was an industry that was sorely in need of better products. During deeper discussions with Kiwi, we uncovered a fierce entrepreneurial spirit and a desire to learn and evolve into a world-class tech leader. Armed with the conviction around a domain-rich entrepreneur and large market opportunity, we decided to proceed forward as a founding investor. Ultimately, the company was formed (spun out of his law firm) at the same time as our initial investment.

Wow, aren’t we delighted that we embarked on this journey? Since being founded in December 2013, the company has grown from minimal revenue to now a successful IPO (NYSE: LAW) with a first trade market capitalization above $2.5B As stupendous this trajectory has been, it neither has been a straight line nor influenced by a single factor. I would attribute the success to a combination of domain strength, grit, collaboration, and good ol’ serendipity.

Domain Strength

Yes, Kiwi’s rich domain expertise was what attracted us to DISCO (N.B., the LiveOak playbook entails backing domain-rich, often first-time entrepreneurs and helping them grow into world-class tech entrepreneurs by helping with all aspects of company building). Kiwi’s obsession with using technology to help lawyers practice law has permeated into a company-wide focus on infusing deep legal knowledge into every piece of code shipped out. Every product was conceived after thinking about the problem from the shoes of a lawyer. As a result, DISCO has fused seemingly orthogonal disciplines of deep understanding of law with world-class engineering to create powerful user experiences that lawyers and other legal professionals love. Lots of entrepreneurs have deep knowledge of their respective fields, but Kiwi and the team exemplified the desire and capability to create magical products – an incredible distinguishing feature of the company. In an industry not known for user delight, the product has an impressive NPS of 63.

Like any other ambitious entrepreneur, Kiwi, even from the first pitch, articulated a multi-stage product roadmap for grabbing a market that was tens of billions of dollars. While that looked like a pipe dream then, today, the company is well on its way to grabbing that exact market he had outlined.

DISCO is very much a story of Kiwi parlaying his rich knowledge of law and thinking many moves ahead for their customers and creating products, services, and experiences to meet current and future needs. That domain-rich inventor’s spirit is what positions this company to define and lead legal tech!

Grit

Kiwi and the company have gotten here in no small measure due to their grit. As with most startups innovating in markets not yet proven, there was some doubt from prospective investors, employees, and so on. They questioned how difficult it may be to attract future investments in legal tech, to show strong traction in the market, whether the business model was right, and the impact of competition, even with the strength of DISCO’s product. Now seeing how far DISCO has come, their uncertainties have not come to fruition. These folks simply underestimated Kiwi and the team’s grit to bludgeon their way through these issues.

The financings of the company certainly involved significant effort. However, through them all, Kiwi never had a moment of self-doubt or reduced conviction on the scale of the company that he could build here. So, for all the entrepreneurs out there, don’t be disheartened if there are challenges in getting the financing dollars and terms you want, as there is not often a ton of term-sheet-love spewing out there.

There were challenges in hiring the optimal leaders for every function, given the preferences around possessing both legal domain knowledge and world-class enterprise software sensibilities. This unique combination is not often available due to the lack of standout winners in legal tech. In absence of optimal leaders, Kiwi has operated as a functional head for practically every department at some point of time. Waiting for the right leaders and gritting it out until the right one was available became the mantra. Today, more than half the executive team are lawyers, and several others have deep backgrounds in the legal industry as well as experience at hyper-growth software companies.

Collaboration

The DISCO success story has also been a textbook example of collaboration between a venture capitalist and an entrepreneur, one that began the day we signed the term sheet. We had finally agreed on all the terms, but that was only after a relatively intense set of discussions where I felt that Kiwi came across as a nitpicky litigator who was focused on corner case scenarios rather than a typical pragmatic tech entrepreneur. I told him to go forward, we needed to be convinced that our relationship could be more collaborative rather than one that felt like a legal scrimmage. Kiwi countered that he would drive over to the office to “make his case.” Now that was a rare icy November day, and he was in Houston, 200 miles away! But that would not deter him from driving to Austin! His action to make this future relationship successful was itself enough of a powerful signal that we signed the deal the moment he strode into our office – that cast the die for a trusting, collaborative style throughout our relationship.

Indeed, we have had many spirited debates – should we stay as a pure-play software business or be full-stack with an AI-based review platform? What is the optimal organizational design to sustain our stunning land and expand model? Should we stay mostly channel vs. make a big push on the direct business? How should we position ourselves (as a vertical software player or as a horizontal software for legal category)? Are we ready to go public – the list goes on and on and on. Every one of these questions had enormous underlying ambiguity and given the magnitude of the consequences, of course, had some fierce opinions on both our sides. Unequivocally, in all these situations, the process was intensely collaborative, intellectually honest, and with the sole emphasis on what was best for DISCO.

It was hard to predict on that icy night in November, I simply could not have hoped for a more collaborative partner than Kiwi on this incredible journey.

Serendipity

The origins of our first investment in the company were serendipitous. We at LiveOak were fortunate that we could spot this “diamond” in the volume of cold emails we received.

Many of the unicorn-esque hires on the leadership team required deep legal and enterprise tech expertise and happened as a result of happenstance. We were so fortunate to find Michael Lafair (a lawyer-turned-CFO). We were also lucky to find Andrew Shimek, a rare lawyer-turned Head of Sales who embodied both legal and enterprise sales traits, and Keith Zoellner, our Head of Engineering with expertise building world-class products and legal domain. Many other people and key board members, such as Jim Offerdahl, Colette Pierce Burnette, and Scott Hill, were connections that were made at the right place, right time.

Finally, it was of course, serendipitous that Kiwi and my favorite soul food cuisine was Sichuan food! Ma-Po Tofu from Mala’s Bistro in Houston or A+A Sichuan in Austin was added motivation to meet, eat and strategize often!

After all, good fortune favors the brave and those with grit!

In closing…

The future is even brighter, and the opportunity is seemingly unbounded, and we believe that the company is indeed poised to be one of the largest and most innovative software leaders for decades to come. This is the first software IPO out of Austin in a while, and it’s extra special given it was birthed in Texas and seed invested at inception by a Texas VC firm.

The success of DISCO and its IPO will be even more impactful for Austin and Texas at large as outsized successes are bound to beget many, many more in the future. Also, with Kiwi and a management team that is committed to building a long-term standalone company, DISCO is bound to have a powerful accelerating effect on the Texas ecosystem. DISCO Cares is a company initiative that is helping drive programs that support vulnerable populations across Texas. There are a number of DISCO-alum startups already sprouting, in Austin and Houston.

Having started this journey as the only other board member besides Kiwi at the time of inception, I am honored to now serve as Chairman of the Board as a part of this milestone IPO event. I look forward to helping Kiwi drive and shape DISCO’s next phase of growth for years to come and to contributing to DISCO’s legacy-shaping initiatives, from their community impact to the spawning of more promising entrepreneurs in the decades to come. In particular, we look forward to partnering with many more entrepreneurs who might learn from and imbibe many of this successful young lawyer’s characteristics around domain strength, grit, and collaboration while building their respective successful ventures!

Our journey with DISCO began with a cold e-mail from Kiwi Camara, which led to our initial investment, and today reached a milestone IPO with a first trade market cap of $2.5B. Our Founding Partner and DISCO Chairman, Krishna Srinivasan, shares an intimate look at this remarkable success story.

We Had To Raise Capital Too…

Seth, our new marketing analyst, asked me a simple question the other day: “with the level of activity in town, why are there not more funds here? What did it take for you guys to raise the first LiveOak fund?”

It was a simple question and one I presumed was obvious to everyone. As we talked more and I told him some of the stories from the process, it became clear that this was something that others would appreciate as well. This blog isn’t a full play by play of the process, but one that intends to give you a flavor for what we went through to raise a new venture capital fund for the Texas market.

First Some Context

The three founders of LiveOak had worked in the venture capital business for over 10 years together at the preeminent venture firm in Texas and had a demonstrable track record. As a result, our expectations were that this would be an easy process. Even more so, we thought that it should take no more than 6 months from the time we left our previous firm. Boy, were we about to get a lesson that we would never forget!

The macro market environment was one of the worst we had seen, with the repercussions from the financial market crisis still reverberating through the system. The public markets had just taken their biggest corrections in a long time. By virtue of focusing on private markets, the venture capital markets took a longer time to feel the full impact of these macro disruptions. The first thing that happened is what is popularly known as the“denominator effect” — since the public markets had corrected aggressively, resulting in shrinking asset bases, the allocation to any asset category gets bigger even when no new investments are made. Allocations to public equity and debt can be adjusted quickly as they are liquid markets, but investments in private equity are long-term and cannot be changed quickly, which results in most limited partners (LPs) finding themselves at or above their desired target allocations (at times even without investing in any new funds). The result is that most LPs at this time were more focused on consolidating their GP relations, not adding to it — definitely not looking for a new fund focused on Texas.

Lastly, all the LPs we knew personally were long-time investors in our former fund and had an established relationship with a Texas-focused firm. They did not need increased exposure in Texas, especially weighing in the denominator effect. This meant we had to find ourselves a completely new set of LPs that would be open to making a bet on the Texas market with a team that was raising a first-time fund in a macro market that was constricting.

If you are asking yourselves, “what in the world made them even try to do this?” you are asking the right question. Looking back on the situation, it seems a bit crazy. Sometimes the only way to do something seemingly impossible is not to know that is what you are up against.

Help. Lots of Help.

Needing to start from scratch without an “installed base” of LPs, we started with those we knew best. We started by calling in every chit we could. Our friends at various other VC firms that had co-invested with us (firms like Lightspeed, Sierra, Matrix, Trinity, NEA, August, and Redpoint) generously walked us through their LP lists and made introductions. While the LPs we knew from our former firm couldn’t invest in our fund, they referred us to others that they thought might have an interest and accepted reference calls for us.

These introductions got us started, but we quickly realized that to make the odds work, we had to cast a significantly wider net. Enter LinkedIn, an aspiring GPs best friend. We looked up every LP we wanted to talk to and found someone that knew them (in some cases, even explored 2nd-level relationships) and asked for introductions. We brute-force cold-called and email pestered until we got an opportunity to present our case for the Texas market and highlight our track record investing in it. Days started and ended with us sitting in the back of Café Uno or Lola Savannah, emailing, calling, or researching LPs and ways to contact them. Sound familiar?

Some Statistics

As I took the long flight to India last week, it gave me the time to take a look at my calendar from the time when we were raising our fund. Here are some back-of-the-napkin statistics for the 18+ month process to bring LiveOak to life. If anything, I bet these stats are conservative as there are meetings my partners took without me, and not everything was meticulously scheduled on our calendars. Nonetheless, here goes:

- At least 46 road trips with an average of 2–3 nights on the road.

- 197 formal in-person meetings — mostly first-time meetings and do not include any follow-up meetings or due-diligence visits.

- I attempted to count calls but gave up very quickly.

- 154 LPs met in person (thousands contacted by email and cold calling). Only 15 of these were LPs that we knew before, so almost 90% of LPs met and presented to were new to us.

While we had our share of visits to New York, Boston, Chicago, and San Francisco, our fundraising also took us to places like Springfield, Illinois (much nicer than you would think and gluten-free friendly!), Albany (beware a pair of Texas VCs driving in a snow storm overnight to make meetings in Boston), St. Louis, Indianapolis, Raleigh, and Charlotte. We even had a trip to Mexico that involved a lot of Tequila tasting. Don’t ask — we were desperate!

Bringing it Together

If you think raising capital for a startup is hard, try raising a fund. Especially, a first-time fund in a recessionary macro environment. The conventional wisdom in fundraising is “get an anchor investor, and it’s downhill from there.” Well, we got ours in Q3 2011. We were then told, “get another large LP, and then it’s really downhill from there” — we did that too in November of 2011. The big difference between raising capital for a company and a fund is driving the process for a large number of investors to show up on the same day and agree to the same set of terms and documents. As a team, we had been involved in a lot of fundraising for our portfolio companies, but this process surprised us more than we expected. It took us over a year from having our two anchor commitments to closing our fund.

As we reflect on the process, a few things stand out to us about the confluence of people, circumstances, and luck that have to come together to support even an experienced team to raise capital. We wouldn’t be here:

- If it were not for an associate at a PE consulting firm that thought we would be a fit for her client and, after months of being unsuccessful at getting their attention, quietly turned us loose on them.

- If it were not for an investment officer at a large pension deciding to try a new process by bringing manager selection in house.

- If it were not for an executive of a large endowment who answered the phone when I cold-called him.

- If it were not for a college roommate who introduced us to the family office that invested in his earlier company.

- And the list goes on…

As we went through this process, we certainly had our days of highs and lows. There were days we were close to throwing in the towel and updating our resumes. The two things that stayed steadfast in this process were the unwavering support of our families and our conviction in the opportunity presented by the Texas market.

A key lesson from this long and arduous process for us was a deep appreciation for what it feels like to be on the other side of the table raising capital. The lack of any response or feedback, the good meetings that went nowhere, taking a meeting and not really listening — we know how that feels. While I will not claim that we are (or will be) perfect in our own interactions with local entrepreneurs, we became determined to put a concerted effort to avoid such experiences. Internally we call our approach “The Entrepreneur’s Bill of Rights” — that’s a topic for a future post.

As we invest the capital we raised, we try not to forget what it took for us to raise it. If it was so hard for a team that had worked together for 10+ years and had over $ 1.5 billion in exits implementing the same strategy in a robust market like Texas to raise the first fund, we can only imagine how hard it will be for others. The only thing that will allow us to raise another fund and invest that here in Texas are the returns we post with this fund, and we are willing to be patient and keep the bar high.

We know we will have to go back and do it again soon (trust me, we are not eager!), and we hope the combination of better macro markets, a resurgent Texas market, and good investment results will make it a bit easier. We hope! And you should too!

Texas Investment Landscape: Dark Ages or a New Beginning

Entrepreneur’s Bill Of Rights

We have been in the venture capital business for over 15 years and one of the issues that continues to be a topic of debate is the expectations of VCs during their interactions with entrepreneurs. We have heard first-hand feedback from entrepreneurs over the years about what they loved and despised in their interactions with VCs. Out of that has evolved a set of values and principles that guide our daily interactions with entrepreneurs.

On one hand there is significant pressure on our time from both existing portfolio companies and the new companies we meet, which exceeds by several orders of magnitude the number of companies we ultimately invest in. On the other hand, the passion and effort put forth by entrepreneurs into their company demand immense respect and focus from us both during and after the interaction in the form of a constructive response with feedback. We believe that managing these demands on time and intensity are critical for us and for the continued thriving of the venture business.

Ironically, the partners at LiveOak felt this pain directly when we were on the road raising our first fund. Most entrepreneurs don’t see this side of our business, but it took more than 18 months with thousands of cold calls to LPs, and hundreds of meetings with prospective investors all over the country. You can read about what it takes to raise a VC fund here. As we debriefed on these meetings and trips, we recalled interactions with certain investors very fondly even when they didn’t invest in our fund. There are other occasions that we do not recall quite as fondly. After successfully raising the fund, we reflected deeply on what we learned from these experiences and the implications on how we would practice our trade as venture investors differently, now on the other side of the table.

The resulting philosophy is what we call the LiveOak Entrepreneur’s Bill of Rights – a set of aspirational goals intended to guide us during our interactions with entrepreneurs.

I. Invest real time: If it is worthwhile for you to invest a big part of your life, it is worthwhile for us to invest 90 minutes to understand it. It takes that much time and often more to appreciate the nuances of an idea and how an entrepreneur’s life journey enables him or her to see the problem and the market opportunity differently when aspiring to disrupt the status quo. Any entrepreneur visiting us with a full pitch deck should expect us to allocate 90 minutes to that discussion – the minimal amount of time we believe that is required to have a rich discussion and develop conviction to want to dig deeper in a next step.

II. No distractions: Those that have pitched to us might find it ironic that a technology venture capitalist is taking notes the old-fashioned way – with pen and paper. You come into our office with the fire, dedication, and grit to pitch your passion. We come in with the intent to provide you with undivided attention. In an electronically-tethered world, we want to remove distractions that would interfere with that interaction – no computers and no cell phones. However, there are always unavoidable situations whether personal or professional that need immediate attention. Those should be extreme exceptions to the rule and in such cases, we tell the entrepreneur to expect this in advance.

III. Timely response: This is the most important and sometimes the hardest thing to do. Most companies fall into three categories by the end of the meeting:

No

The No’s are taken care of quickly because we often inform the entrepreneur unambiguously at the end of the meeting if the opportunity does not fit our investment interest or what additional metrics and data are needed before we would consider revisiting the company. Other times we reaffirm our initial assessment with the other Partners and respond back to the entrepreneur within a week through a call or email explaining there is no possibility we will invest.

Yes

The second category is also relatively straightforward since it involves additional due- diligence and introductions to the rest of the partnership.

Not sure yet

It is the last and hardest category. Sometimes it means waiting for the story to develop; other times we need to identify an expert in our network that knows the market better. In these situations, it is our goal to keep the entrepreneur informed of the process and move the company to a clear yes or no as soon as possible.

There are certainly times when, in our minds, we respond with a decision and pointed feedback on what it would take for a company to be investment worthy, but may not come across as a definitive answer in the entrepreneur’s eyes. If you ever encounter the feeling of not knowing which of the three categories you fall under, we urge you to reach out and ask for clarification. While we recognize we will not bat a thousand in every entrepreneur’s eyes, this is one that we actively continue to improve both as individual investors and as a firm.

IV. Be helpful even if we are unable to invest: Any company we meet not only has the potential to impact the Texas ecosystem, but the world as well. Regardless of whether or not this impact is made inside of the LiveOak portfolio; we strive to be helpful in any and all ways that we see fit. Sometimes this means a tough critique on what areas to prioritize and develop further. For others it means making a connection within our network. We realize our long-term success is defined by the success of the Texas ecosystem and we are fully committed to help accomplish that.

We will be the first to admit that we aren’t perfect and that adhering to the LiveOak Entrepreneur’s Bill of Rights requires constant and conscious effort. However, having been in this business for 15+ years and recently sitting on your side of the table, what should not be in doubt is our sincere desire to use it as the North Star that guides our behavior. Our legacy as a firm will be measured not only by the returns our investments deliver to our investors, but also by the impression we leave and influence we have on every entrepreneur we meet.

This is the ethos that will steer LiveOak in the years (and funds) to come.